Blockchain

Blockchain’s Impact on Global Financial Inclusion Efforts

As the world hurtles toward a more digital and interconnected future, blockchain technology is emerging as a transformative force in the financial sector. Its potential to enhance global financial inclusion is one of its most revolutionary impacts. Let’s explore how blockchain plays a pivotal role in bridging financial gaps and providing opportunities for millions worldwide who remain underserved by traditional banking systems.

Understanding Blockchain Technology

At its core, blockchain is a decentralized digital ledger that records transactions across a network of computers. This ledger is inherently secure and tamper-proof, making it an ideal solution for financial applications. By eliminating the need for intermediaries, blockchain reduces costs and increases efficiency in financial transactions. This technology is particularly relevant for individuals lacking access to conventional banking services, offering a streamlined and accessible alternative.

Eliminating Barriers to Banking

Challenges in Traditional Banking

Traditional banking systems often fail to serve individuals in remote locations or those without requisite documentation. Costs related to opening and maintaining bank accounts can also be prohibitive, creating a significant barrier. Moreover, the reliance on physical infrastructure limits the reach of traditional banks to rural or underserved communities.

Blockchain as a Solution

Blockchain provides an alternative by enabling digital identities and financial transactions that are not reliant on physical documents or proximity to a bank branch. Through blockchain-powered platforms, individuals can access banking services on their mobile devices, thus transcending geographical limitations and drastically reducing the entry threshold for financial inclusion.

Facilitating Safe and Secure Transactions

One of the hallmarks of blockchain technology is its enhanced security features. Transactions made using blockchain are encrypted and validated by the network, ensuring transparency and minimizing the risk of fraud and manipulation. This reliability is crucial for populations who have traditionally been cautious of engaging with financial institutions due to trust issues.

Enabling Micropayments and Microfinancing

Micropayments

Blockchain facilitates the seamless processing of micropayments, which opens up new avenues of financial activity for low-income earners. By reducing transaction costs, blockchain technology makes it economically viable to conduct small-value transactions, thereby supporting everyday financial transactions that are essential for underserved communities.

Microfinancing Opportunities

Through blockchain, peer-to-peer lending platforms are increasingly becoming popular, offering microloans to entrepreneurs and small business owners without the need for a traditional credit history. By utilizing smart contracts, blockchain can effectively verify and execute loans automatically, reducing the overhead costs associated with microfinancing.

Cross-Border Transactions Made Simple

Blockchain technology provides a novel solution to the often-complex process of cross-border transactions. Traditional remittance channels are plagued by high fees and lengthy processing times. Blockchain offers a more efficient system where transactions can be completed quickly and at a fraction of the cost, thus empowering migrant workers and their families relying on remittances.

The Future of Financial Inclusion with Blockchain

As blockchain technology continues to evolve, its potential to drive financial inclusion becomes even more apparent. Innovative applications such as decentralized finance (DeFi) are emerging, offering a host of financial products and services powered by blockchain technology. These products are paving the way for greater financial accessibility, flexibility, and empowerment for marginalized communities around the globe.

In conclusion, blockchain technology is setting the stage for a more equitable financial future by breaking down longstanding barriers and expanding access to vital banking services. As adoption increases, blockchain’s role in fostering global financial inclusion will likely grow, offering a promising pathway towards an inclusive global economy.

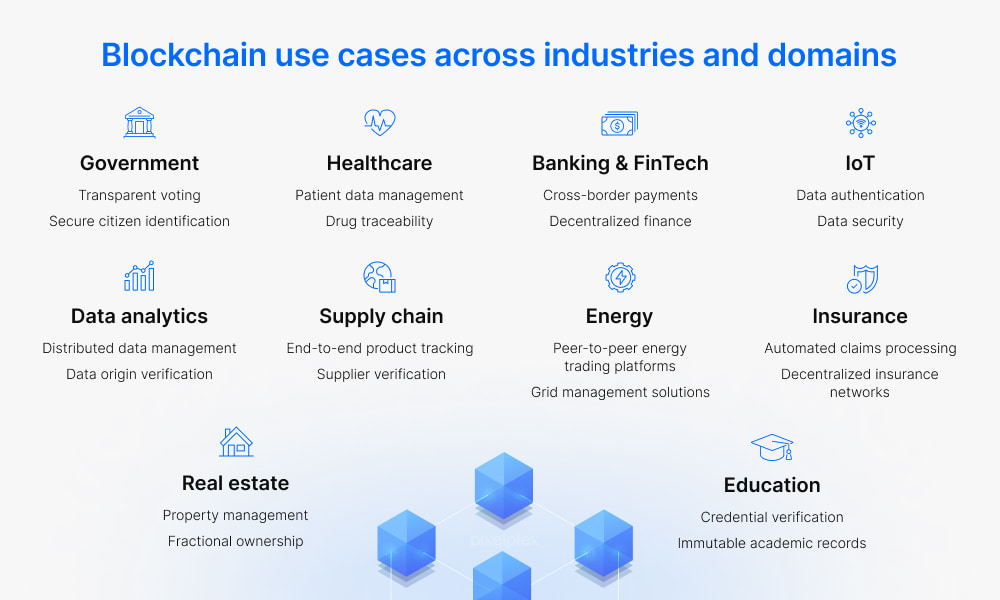

Top 5 Blockchain Use Cases Transforming Business in 2026

Blockchain technology has moved far beyond cryptocurrency. In 2026, businesses across industries are leveraging distributed ledger technology to solve real-world problems with transparency and security.

1. Supply Chain Management

Blockchain enables end-to-end visibility in supply chains. Companies can track products from manufacturer to consumer, reducing fraud and ensuring authenticity.

2. Smart Contracts

Self-executing contracts eliminate the need for intermediaries. Legal agreements, insurance claims, and real estate transactions are being automated through smart contracts.

3. Healthcare Records

Patient data stored on blockchain gives individuals control over their medical history while ensuring data integrity across hospitals and clinics.

4. Digital Identity Verification

Blockchain-based identity systems reduce identity theft and streamline KYC processes for banks and financial institutions.

5. Decentralized Finance

DeFi platforms are disrupting traditional banking by offering lending, borrowing, and trading without centralized institutions.

Blockchain is no longer a buzzword. It is a foundational technology reshaping how businesses operate in the digital age.

Top 5 Blockchain Use Cases Transforming Business in 2026

Blockchain technology has moved far beyond cryptocurrency. In 2026, businesses across industries are leveraging distributed ledger technology to solve real-world problems with transparency and security.

1. Supply Chain Management

Blockchain enables end-to-end visibility in supply chains. Companies can track products from manufacturer to consumer, reducing fraud and ensuring authenticity.

2. Smart Contracts

Self-executing contracts eliminate the need for intermediaries. Legal agreements, insurance claims, and real estate transactions are being automated through smart contracts.

3. Healthcare Records

Patient data stored on blockchain gives individuals control over their medical history while ensuring data integrity across hospitals and clinics.

4. Digital Identity Verification

Blockchain-based identity systems reduce identity theft and streamline KYC processes for banks and financial institutions.

5. Decentralized Finance

DeFi platforms are disrupting traditional banking by offering lending, borrowing, and trading without centralized institutions.

Blockchain is no longer a buzzword. It is a foundational technology reshaping how businesses operate in the digital age.

The global supply chain industry confronts numerous challenges, and transparency stands as one of its most pressing issues. The integration of blockchain technology offers groundbreaking ways to enhance transparency across supply chains, promising improved efficiency, accountability, and trust among stakeholders.

Understanding Blockchain Technology

At its core, blockchain is a distributed ledger technology that records transactions across multiple computer systems in a way that ensures security and transparency. Its decentralized nature ensures that no single entity controls the data, making it resistant to tampering and fraud. By applying blockchain to supply chains, companies can achieve unparalleled visibility into their operations.

Improving Traceability and Accountability

Real-Time Tracking

Blockchain allows for real-time tracking of products from their origin to the final consumer. With unique digital identities assigned to each batch or component, stakeholders can follow products at every stage of the supply chain. This ensures accountability as every transaction is recorded and immutable.

Enhanced Product Authenticity

Consumers today demand to know the origins of the products they purchase, especially in sectors like food, pharmaceuticals, and luxury goods. Blockchain provides an unalterable record of a product’s journey, helping to verify its authenticity and build consumer trust.

Streamlining Logistics and Efficiency

Automated Processes

By integrating smart contracts, which are self-executing contracts with the terms written into code, blockchain can automate numerous logistics processes. This not only reduces the time required to complete transactions but also minimizes human error, resulting in increased overall efficiency.

Reduced Costs

With improved transparency and decreased reliance on intermediaries, blockchain technology can help reduce costs significantly. The streamlined processes enabled by blockchain lower administrative expenses and enhance transaction speeds, leading to a more cost-effective supply chain operation.

Ensuring Data Security and Integrity

Data breaches and security concerns are prevalent issues in supply chain management. Blockchain’s cryptographic and decentralized nature ensures that data remains secure, with participants only able to view the transactions they are authorized to see. Furthermore, once data is entered into the blockchain, it cannot be altered without consensus from the network, ensuring data integrity and trust.

Challenges and Considerations

Scalability Issues

Despite its advantages, blockchain technology must overcome scalability issues to handle the vast number of transactions occurring in global supply chains. Continuous development in blockchain technology aims to address these limitations, but they remain a significant hurdle to widespread adoption.

Regulatory Compliance

Navigating the regulatory landscape poses challenges for blockchain in supply chains. Different countries and regions have varying regulations regarding data privacy and digital transactions, which can complicate blockchain implementation. Businesses must ensure compliance with these regulations to successfully integrate blockchain into their supply chains.

As we navigate the future of supply chain management, the role of blockchain technology continues to become more prominent. By enhancing transparency, implementing efficient processes, and ensuring security, blockchain has the potential to revolutionize supply chains globally, offering greater insights and control over the complex ecosystems of production and distribution.

Top 5 Blockchain Use Cases Transforming Business in 2026

Best SEO Link Building Strategies for 2026 Part 2

Best SEO Link Building Strategies for 2026

Best SEO Link Building Strategies for 2026

Accessily Review: An Honest Look at Its Guest Posting Marketplace

LinkHouse vs Adsy: Which Guest Posting Service Is Worth Your Budget?

Top 5 Blockchain Use Cases Transforming Business in 2026

Top 5 Blockchain Use Cases Transforming Business in 2026

Best SEO Link Building Strategies for 2026

Best SEO Link Building Strategies for 2026

Getfluence vs WhitePress: Which Platform Is Better for Premium Publisher Outreach?

Test Auto Publish Google Doc Post 2

Top Marketing Automation Tools to Watch in 2025

Cloud-Native Applications: Why They’re Essential for Today’s Enterprises

The Rise of Subscription-Based E-commerce Models

How Zero Trust Models are Revolutionizing Cybersecurity

The Role of Blockchain in Enhancing Supply Chain Transparency

How AI is Changing the Face of Cloud Computing

Navigating the Aftermath of a Data Breach in Today’s Digital Age

Exploring the Environmental Impacts of Blockchain Technology

Choosing the Right Web Hosting Plan for Your Start-up: A Comprehensive Guide

The Role of AI in Predicting Future Cyber Threats

Emerging Trends in Web Hosting: What to Expect in 2025

Exploring the Environmental Impacts of Blockchain Technology

The Future of Real Estate Transactions with Smart Contracts

Leveraging Augmented Reality to Enhance the Online Shopping Experience

The Impact of Cryptocurrency on E-commerce Payment Solutions

How AI is Changing the Face of Cloud Computing

The Impact of Edge Computing on Cloud Services

Blockchain’s Impact on Global Financial Inclusion Efforts

How User-Generated Content is Shaping Brand Authenticity

Exploring the Benefits of Cloud-Based Web Hosting Solutions

Best Practices for Securing Your Remote Workforce in 2025

How Blockchain is Transforming the Gaming Industry

2025 Trends in Cloud Security: Keeping Your Data Safe

Navigating the Aftermath of a Data Breach in Today’s Digital Age

Cloud-Native Applications: Why They’re Essential for Today’s Enterprises

Top Marketing Automation Tools to Watch in 2025

Data-Driven Marketing: Harnessing Analytics for Better Outcomes

How Social Commerce is Changing E-commerce Strategies

-

Web Hosting2 years ago

Web Hosting2 years agoChoosing the Right Web Hosting Plan for Your Start-up: A Comprehensive Guide

-

Cybersecurity2 years ago

Cybersecurity2 years agoThe Role of AI in Predicting Future Cyber Threats

-

Web Hosting1 year ago

Web Hosting1 year agoEmerging Trends in Web Hosting: What to Expect in 2025

-

Blockchain1 year ago

Blockchain1 year agoExploring the Environmental Impacts of Blockchain Technology

-

Blockchain1 year ago

Blockchain1 year agoThe Future of Real Estate Transactions with Smart Contracts

-

E-commerce2 years ago

E-commerce2 years agoLeveraging Augmented Reality to Enhance the Online Shopping Experience

-

E-commerce1 year ago

E-commerce1 year agoThe Impact of Cryptocurrency on E-commerce Payment Solutions

-

Cloud Computing1 year ago

Cloud Computing1 year agoHow AI is Changing the Face of Cloud Computing